PS: It is a descriptive post. Suggest reading it entirely to understand the depth.

Well traffic is an overused and over abused word in Bangalore. It’s

been 3 years and am in love with the city. Good people, excellent weather,

happening night life, lazy brunches in cafés, it’s got everything you ask for.

But getting to all these places that is a task in itself. When you are told you

need to get somewhere in Bangalore a word starting with "F" comes to

your mind. Well its fear, absolute fear of getting stuck in the road for hours.

It's like Lord Kitchener pointing that finger at you in the famous WW-1 poster

saying "You" are responsible for this traffic.

Yesterday however was a revelation. When I woke up in the

morning to step out for work Google now told me it will take me 10 minutes less

than usual because of "less traffic". Wow! Indian festivals have that

impact. I immediately got into the Vettel mode and my humble Chevy beat

suddenly looked like a Red bull racing mean machine. A slight drizzle ensured

that the weather was at its best! The beat over the week has seen only the

first 3 gears during my commute and the 4 gear seemed like a candidate waiting for

his interview turn. The fifth gear, well was next to non-existent.

Today however I had decided to push her and beat the clock to

work. As always Google was right, traffic was less and the roads were free with

a slight drizzle just enough to keep the roads wet. I revved my engine and the

beat responded as if it’s been woken up after ages. I kept the engine on boil

between 2-3k rpm continuously and the little Chevy was upto the game. She was

charging well on the wet roads with a hint of under steer maybe because of the

wet road and the fact that I was pushing the car. We hit the ring road and for

the first time in ages hit a ton on that road and soon enough I spotted a speed

breaker which on normal days was obsolete because there was no speed and seemed

like a hump. I braked and expected a rally like jump over it, but was surprised

how the little beat managed to hold ground not lose traction on a significantly

wet road and yet come to a respectable 20 kmph within seconds and soon enough

to not mess with the speed breaker. I was amazed and impressed at this little

car's capability which I had never noticed on a normal day. I decided to test

it a little more and revved again after the speed breaker. The 1.2 litre motor responded

and I was able to hit a ton again. The mid-range is not that good but today I

got to explore the top end of the car which I have never experienced over the

past 3 years because I never got the chance. As these thoughts were flowing in

my head I clearly missed a huge puddle right at the exit of the flyover. The

beat hit the puddle at 90 and I hung on. Again yet another surprise, the Chevy

held on and didn't lose the straight line stability. It transferred the

feedback via the steering that I had messed up but didn't let the car get disturbed.

This was amazing because the puddle was deep enough to reach above my fog lamps

and I was sure that there would be some damage to the bumper. With a heavy

heart I got down to check the bumper and found it to be intact as if nothing

happened. Well when I was told in most of the meetings with the dealer about

the build quality of Beat which at that point pointless theory without

experience. Today I got to see it and experience it - and was amazed at what

this little Chevy pulled out.

I settled into a saner sort of driving and started thinking,

this is a company which pioneered in safety and introduced stuff like seat

belts which changed the course of automotive history and made cars for more

than 100 years, then why is it failing in India? I have read testimonials of

customers who have walked out of crashes unscarred because of Chevy's build

quality and safety and have seen customers give high regard to Chevy for the

way they are built and for the legacy. But I feel Chevy has ignored India as a market

when other players have focussed well on the sub-continent. Let’s see the

current scenario for the American Automaker –

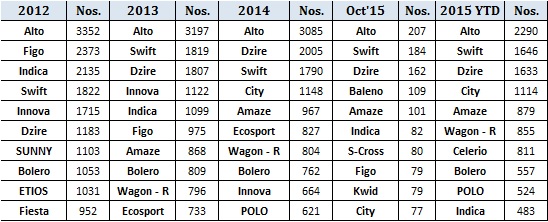

|

| Sales Trend - Chevrolet in India |

Chevy’s sales have dropped 48% in year 2014 when compared to year

2011. Based on current sales (31528 units till Oct’15) and forecast this year,

we expect GM to close at ~38000 units which will lead to a 66% drop vis-à-vis 2011!

But what has led to such decline for an Iconic Brand which had enviable status

in India at a particular time:

·

One of the oldest Automobile Companies in the world (as of date,

it is 104 years old!)

·

First Automobile Company to open an Assembly Plant in India (way

back in 1928!)

·

Chevy vehicles were widely featured in early Bollywood movies

(most famous were the Impala’s) and helped Chevrolet to gain a premium status

in Indian consumers mind

·

Chevy was a global marque and had immensely helped GM to remain

the No.1 Car Maker for 77 years in a row! (until Toyota snatched the top spot)

·

Chevrolet was the key to GM’s revival hopes in India and had

shown potential initially

·

Spark, Beat & Tavera were once known to be the benchmark in

their respective segments

·

One of the few automakers to have a product in every segment

(Spark – Entry level hatchback, Beat – Mid-hatchback, Sail UVA - premium hatch,

Sail NB – Sedan, Tavera & Enjoy – MUV, Cruze – premium Sedan, Captiva/now

Trailblazer – SUV)

·

Extensive network in India – Over 260 dealerships and similar number

of Workshops!

So with these many advantages, what went wrong?

Ø

Multiple failed products – Actually terming these products as

failures would be unfair, however GM pulling over these products from the

portfolio backfired (Opel Astra, Opel Corsa, Opel Corsa Sail, Chevrolet Aveo,

Chevrolet Aveo-UVA, Chevrolet Forester, Chevrolet Optra)

Ø

Negative Word of Mouth – Once the aforementioned products were stopped,

the existing owners faced trouble in servicing, availability of spares and

finally the resale value. Though the owners were extremely happy with the

performance of their cars, long-term ownership experience was jittery

Ø

No Unique Brand Philosophy – Though Chevy had an American DNA,

the products didn’t - Spark, Beat and Captiva were designed by Daewoo/GM Korea;

Sail and Enjoy were SAIC (GM China) offerings, Tavera was nothing but a

rebadged Isuzu!

Ø

Dismal Dealership Experience – The dealerships were not standard

across and the lacklustre sales attitude cost them dearly with the loss of

customer faith and trust. The dealer infrastructure as well in many cases were

not projecting the premium brand image that otherwise was required.

Ø

Improper Product Planning – Beat was an extremely promising

product when it was launched and performed impressively for quite some time.

However, no major updates on the brand made it lose steam in the Indian market

and sales went down bottom. The story remains the same for Tavera, Cruze, etc.

Also the manufacturer’s incapability of bringing India specific products led to

the downfall

Ø

High Maintenance & Serviceability Concerns – A frequent

concern shared by Chevy customers. Though Chevrolet did mega campaigning in the

name of Chevrolet Promise to highlight low maintenance; the customers weren’t

impressed.

Ø

Product Issues & Intermittent Recalls – Issues related to

brakes, clutch, etc were common in the new offerings. Also the recall of Sail

within first 6 months itself impacted the brand negatively. Tavera emission

goof up added to the despair.

Ø

Over Discounted Brand – The brand ads started looking like a grocery

shop ad with discounts on ALL its product range! The theme lost appeal on the

product characteristics and in a while meant demeaning in overall.

Ø

Low Survey Ratings – As per the latest 2015 JD Power Survey

report, Chevrolet stood last in Sales Satisfaction and 8th in

Service Satisfaction!

Recently GM has shown promise to invest even higher in India and

work towards increasing its Market Share in the sub-continent. So what will

work for this cult yet damaged brand –

§

1 Blockbuster Model – Indian consumer these days forgive very

easily. Learn something from your fellow American (Ford). Ecosport did the

magic initially and now they’ve brought Aspire & New Figo. That 1 crucial

mass product will prove to be the breakthrough to initiate the repair of Indian

Operations

§

Revamp Dealership Network – We appreciate the Automakers

decision to cut down dealers (though we are still unaware if the good dealers

are also lost). However, the dealer network needs to be supported to standardize

their infrastructure and workshops.

§

Connect with the Existing Customers – Chevy owns a handsome

number of customers already and has to make the connection much stronger. So an

over-dedicated Customer Care team and super-natural customer connect

initiatives are the need of the hour.

§

American DNA + Indian Usage – Right combination to win the

Indian Consumer. Though, this combination doesn’t mean to bring American Gas

Guzzlers to India (name Trailblazer). We need funky looking car, with acres of

space inside, run miles with great efficiency, have loads of features and costs

less as well.

§

Aggressive campaigning of Chevrolet Promise – Yes, the brand did

see some positivity when Late Karl Slym assured customers of low maintenance

when the program was launched. The campaign dwindled and neither Chevy nor

dealers seem interested. Can we have Mr. Arvind Saxena lead the charge and overhaul

the campaign?

§

Focus on ALL models – There was a time when Spark caught up well

in the Indian market and Beat was launched. Chevy’s entire focus on Beat,

slowed down the Spark and today Spark is off the shelf! The story remains

similar for the remaining portfolio and the varying focus by the OEM have

killed some potent products. Hence, focus on the ENTIRE portfolio is required

to make it big in India.

If

only Chevy had paid more attention to India, and given India specific products

by using their vast know how of the industry, we would have seen a different

Chevrolet in India. Hope the revival that Mary Barra has been speaking about

has all this. Till then am happy with my little Chevy Beat but always concerned

as to what will happen if God forbid something goes wrong and I have to replace

some part. Till then good luck Chevy and hopefully you will get your act

straight and not fade away!!!

(Author's Profile: Manu Sasidharan. Am a hardcore petrol head, an auto enthusiast and an amateur designer. I have been in close touch with the industry for a long time and am abreast with the action in the automotive sphere. Driving is my passion and combined with a love for travelling makes me a nomad by nature. On the education front, I have done my Engg in Electrical and Electronics from Cochin university and my Management studies from Symbiosis Pune.)